A question frequently asked by taxpayers is whether or not the proceeds from a lawsuit must be included in their taxable income. The answer is the taxation of your settlement proceeds will focus on the different categories of income that your payment is broken down into.

Below are the six categories:

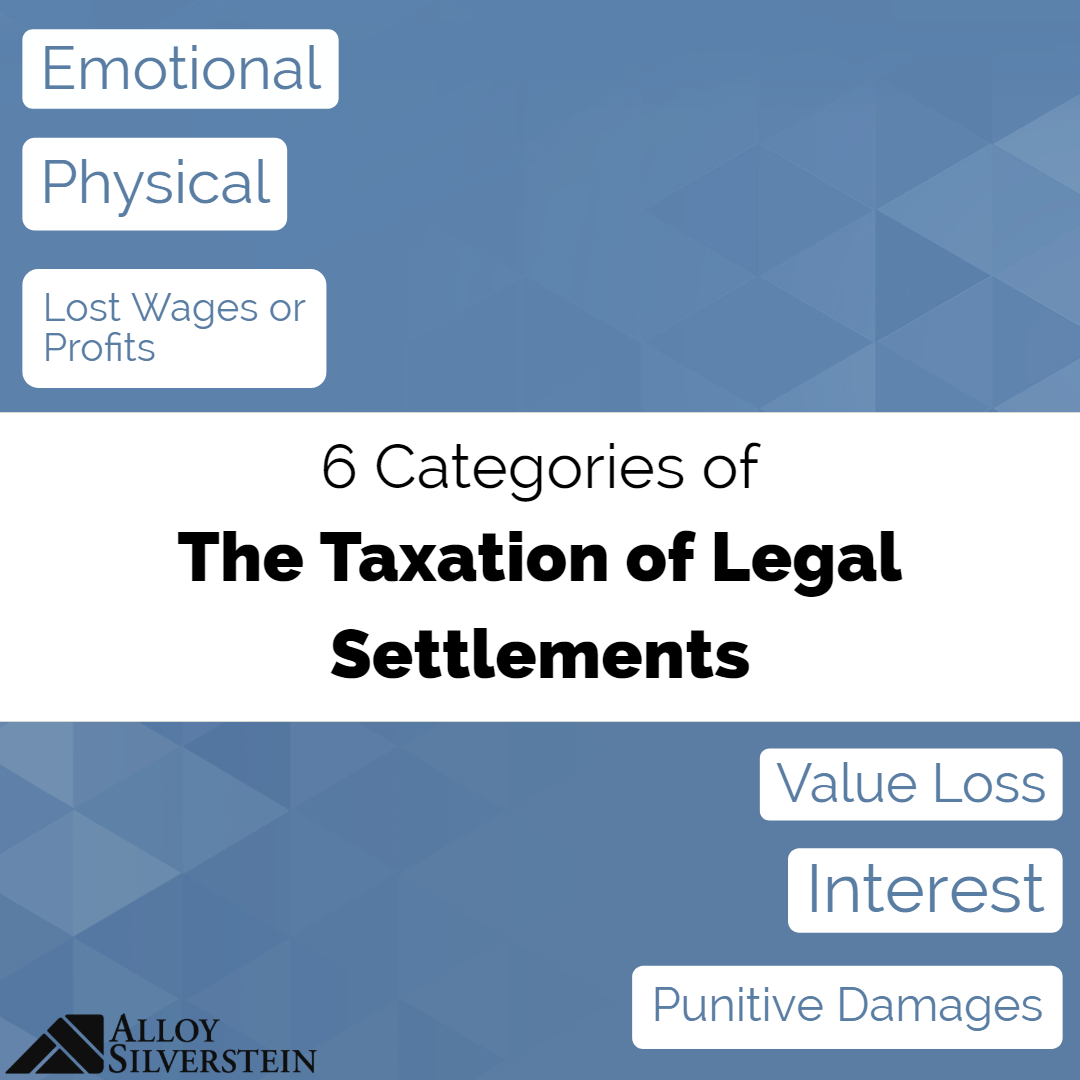

Any proceeds received for emotional distress that do not original from a physical injury or physical sickness would be taxable. If related to a physical injury or physical sickness, the proceeds would not be subject to tax. The amounts you receive could potentially be reduced by related medical expenses paid that you did not deduct or get a tax benefit for.

Payments received for a personal physical injury or physical sickness are not considered taxable income if you did not tax a medical expense deduction in prior years for the injury/sickness. If you did tax a deduction and received a tax benefit, that portion would be taxable. If it is over the course of multiple years, you would need to allocate the income on a pro rata basis.

The portion of any proceeds related to lost wages or lost profits would be taxed the same as your normal wages/profits.

Any interest associated with an award or settlement will always be considered taxable.

These almost always included in your taxable income even if related to personal physical injuries or physical sickness. In some cases, if the state statues only allow wrongful death claims to be award punitive damages it would not be taxable.

Proceeds received to for loss in value of property would only be taxable if the amount is higher than your adjusted basis in the property as the excess would be considered income. If the settlement is less than your adjusted basis, you would reduce your basis in the property by the proceeds amount you receive.

The attorney fees you incur are allowed to be deducted. Unfortunately, the new tax law eliminated the miscellaneous itemized deductions starting with the 2018 tax year. This means that unless the taxpayer receiving the money is a business, the attorney fees cannot be deducted. More importantly, if you were awarded taxable and non-taxable income from the case, the attorney fees need to be broken up in the same ratio and only the taxable percentage can be deducted.

It is important to note that the specific circumstances of one taxpayer’s resolution may not be the same as another. This is a general guide that can be used to help understand how an award or settlement may be taxed at a federal level. Ultimately, when receiving a legal settlement or award, you should consider contacting a tax professional so they can guide you through the resolution and help determine state taxability as some states may not follow federal law.

Associate Partner

Chris provides accounting, tax planning, and consulting services to professional athletes, family entertainment centers, and other businesses in the amusement and hospitality industry. He also aids clients in implementing cloud accounting solutions.

View Chris's Bio → Follow @AthleteCPA on Twitter →